Flusso handles the work your raise actually requires — investor narrative, targeting, outreach, pipeline management, and close — so you can keep building the company that makes the raise worth doing.

Begin the ProcessA serious raise is a hundred-plus hours a month of disciplined process. Your company already takes a hundred-plus hours a month. The math doesn't work. Something gives. A raise run alongside a company can't run with the consistency a raise actually requires.

By the time the round closes, the company has slowed and the founder is exhausted. The raise that was supposed to fund growth has cost six months of growth instead. The cost is rarely calculated honestly. It's almost always larger than founders expect.

These are not aspirational. They are the engagement — written into the contract, tracked weekly, and delivered every month.

Every introduction is to a verified-fit investor with confirmed interest. Warm introductions, not a list of names.

Thirty minutes, every week, to review pipeline status, walk through active conversations, and align on the week ahead.

Every investor contacted, every response received, every meeting booked. In writing. So you always know where the raise stands.

Reachable when the raise needs an answer, not at next week's call. Same-day responses through the channels you already use.

As conversations progress and objections surface, we refine the framing in real time. The pitch sharpens with every meeting.

Cumulative outreach, pipeline progression, and strategic adjustments. So the raise compounds instead of drifting.

The difference between a founder-led raise and a Flusso-led raise isn't theoretical. It shows up in six places — every time.

Flusso doesn't hand you tools to run the raise faster. We run it. The function that would otherwise sit on your desk (investor research, outreach, pipeline management, follow-up) moves off your desk and stays off.

A cold email from an unknown founder waits in a queue with hundreds of others. A warm introduction from a trusted source gets opened, read, and replied to. The raise moves through faster doors.

Investors price risk the moment a deal hits their desk. Arriving through an intermediary signals that the process is serious, and their time won't be wasted. That signal reorders how they engage.

The same company can be framed as a risky bet or a category leader depending on how the case is built. We position your deal as the version investors are already looking to fund.

We know which investors are deploying now, who passed on similar deals last quarter, and what objections are landing in the market today. That intelligence sits behind every targeting call we make.

Most rounds don't fail at the pitch. They fail at the close: when momentum stalls, decisions drift, and verbal commitments quietly evaporate. We govern the close as its own discipline. Commitments become wires.

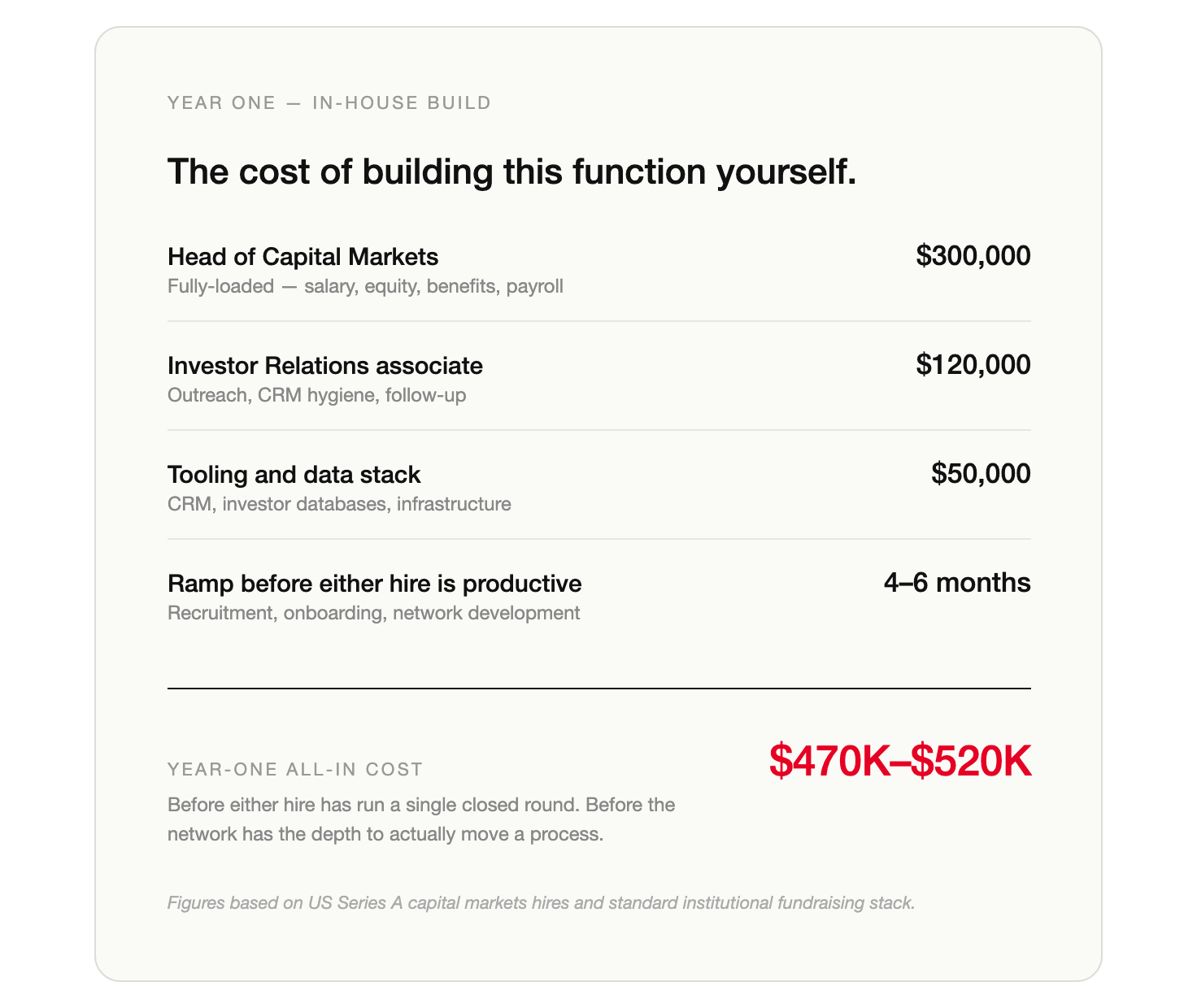

Running the raise yourself is where almost every founder starts. It works for some time, then the raise management starts to compete with the company itself. The next thought is usually to hire for it. A Head of Capital Markets to own the function. An IR associate to run the operational layer. The numbers on the right are what that actually costs.

Flusso is the version of that function that already exists — assembled, calibrated, and inside the relationships. Plugged in for the raise. For a fraction of what building it costs, and only while you're actively raising.

The capital advisory industry has trained founders to expect three things: a large upfront fee, equity dilution, and a back-end success fee that compounds the cost.

Many firms charge a percentage of the raise before work begins. We don't take an upfront cut of capital that hasn't been raised yet.

Advisors who take equity are buying into your cap table on the day you have the least leverage. We stay out of it. Your ownership remains yours.

You don't pay an attorney only when they win the trial. You don't pay a surgeon only when the operation succeeds. You pay for the work. The hundreds of hours of expertise applied to a difficult problem, where the outcome depends on factors no professional can fully control.

A serious institutional raise is the same kind of work. None of that effort changes based on whether the founder closes the round. Investor decisions, pitch performance, negotiations — these sit with the founder and the market, not with us.

Asking us to absorb 100% of the downside risk on variables we don't control isn't a fee structure. It's a full transfer of risk. Firms that quote success-only know this. They take it on volume, with thin senior involvement, betting that one or two deals in fifty will close enough to subsidize the rest.

The other founders get a marketing pipeline pretending to be a fundraising process. The fee structure exists to protect the quality of the raise — which is the thing the founder came here for in the first place.

We don't take on every raise that comes through the door. The work is too involved and our reputation with investors is too important to compromise on either end.

If you're on the left side of this list, the next step is the intake below.

Complete the intake form. We review every submission.

If there's a fit, we'll be in contact to schedule an initial assessment.